The Point-in-Time Inventory This is the best-known and most widely used form of inventory taking: The entire inventory is physically counted on a specific cutoff date—usually the balance sheet date. This article explains the definition, legal basis, procedure, and deadlines for cutoff-date inventory, as well as its advantages and disadvantages.

In the Point-in-Time Inventory All of a company's assets are recorded in terms of quantity and value as of a single, specified reporting date. The date used is usually the Balance Sheet Date (often December 31). The inventory calculated in this way is included directly in the financial statements.

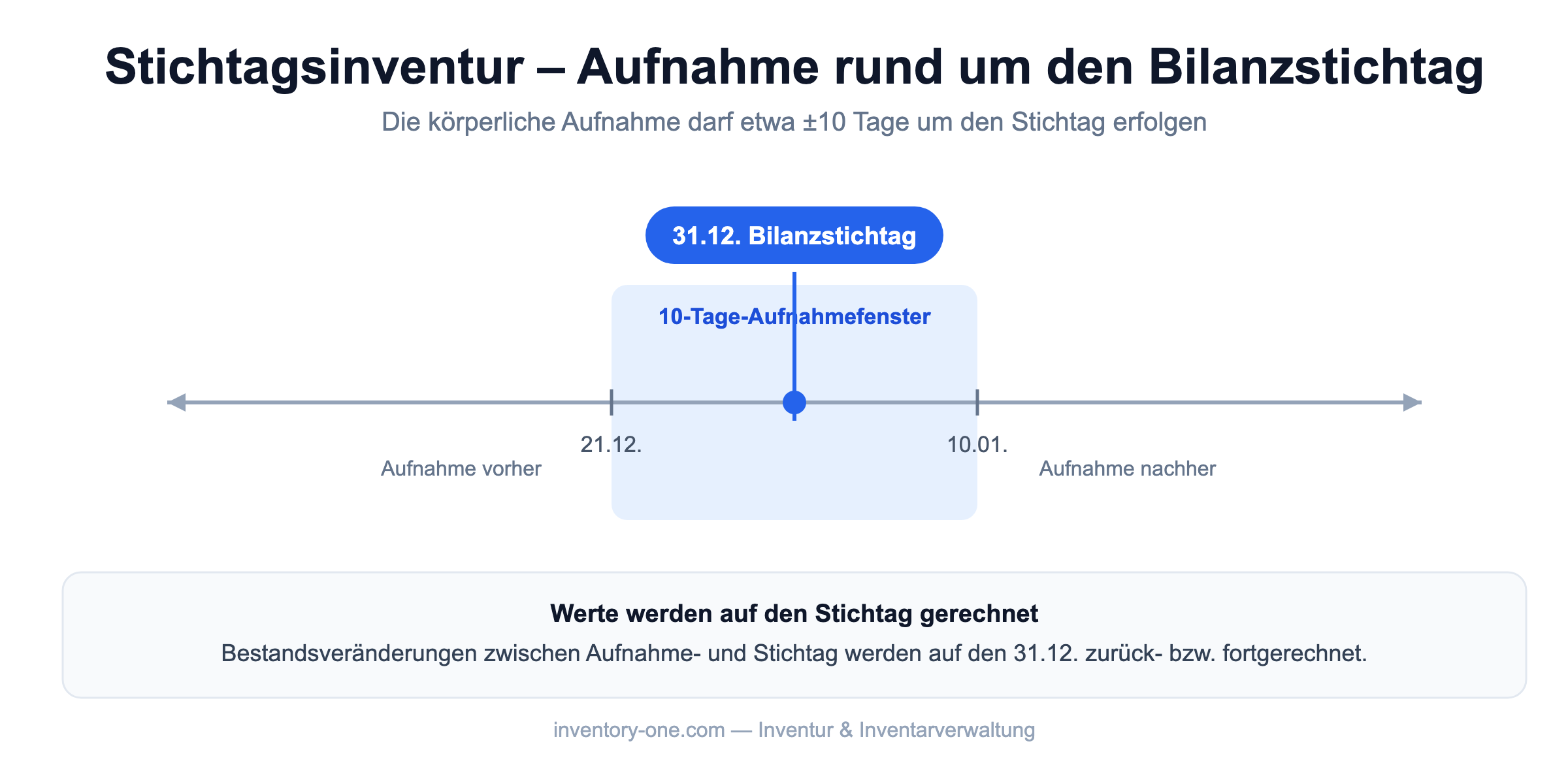

The requirement to conduct an inventory arises from § 240 HGB. For practical reasons, the count does not have to be taken exactly on the cutoff date: The tax authorities accept a physical inventory taken within approximately ten days before or after the deadline. Changes in inventory between the date of entry and the reporting date are adjusted forward or backward to the reporting date in terms of both quantity and value.

If you want to avoid the peak workload at the end of the year, you can switch to a continuous or staggered inventory. You can find a complete comparison of all methods in our overview of inventory types.

Speed is key to data quality, especially during a point-in-time inventory. With mobile data collection via an app, multiple teams can count inventory simultaneously and enter the data directly into the system—without paper forms or manual data entry.

With Inventory ONE Record inventory using Barcode or QR Code Scan, the Mobile Inventory Count via App processed directly at the warehouse and received audit-compliant records at the touch of a button. Learn more on our pages about Inventory Software and Inventory management.

As of the balance sheet date, which is usually December 31. The physical examination may take place approximately ten days before or after the balance sheet date.

In a point-in-time inventory, everything is counted on the inventory date; in a continuous inventory, the counting is spread out over the entire year, and on the inventory date, a book inventory is sufficient.

No. It is a permissible method of taking inventory, but companies may also choose other methods in accordance with Section 241 of the German Commercial Code (HGB).

This post is part of our series on inventory types. Here you'll find all related articles:

About 10,000 satisfied users Trust in Inventory ONE